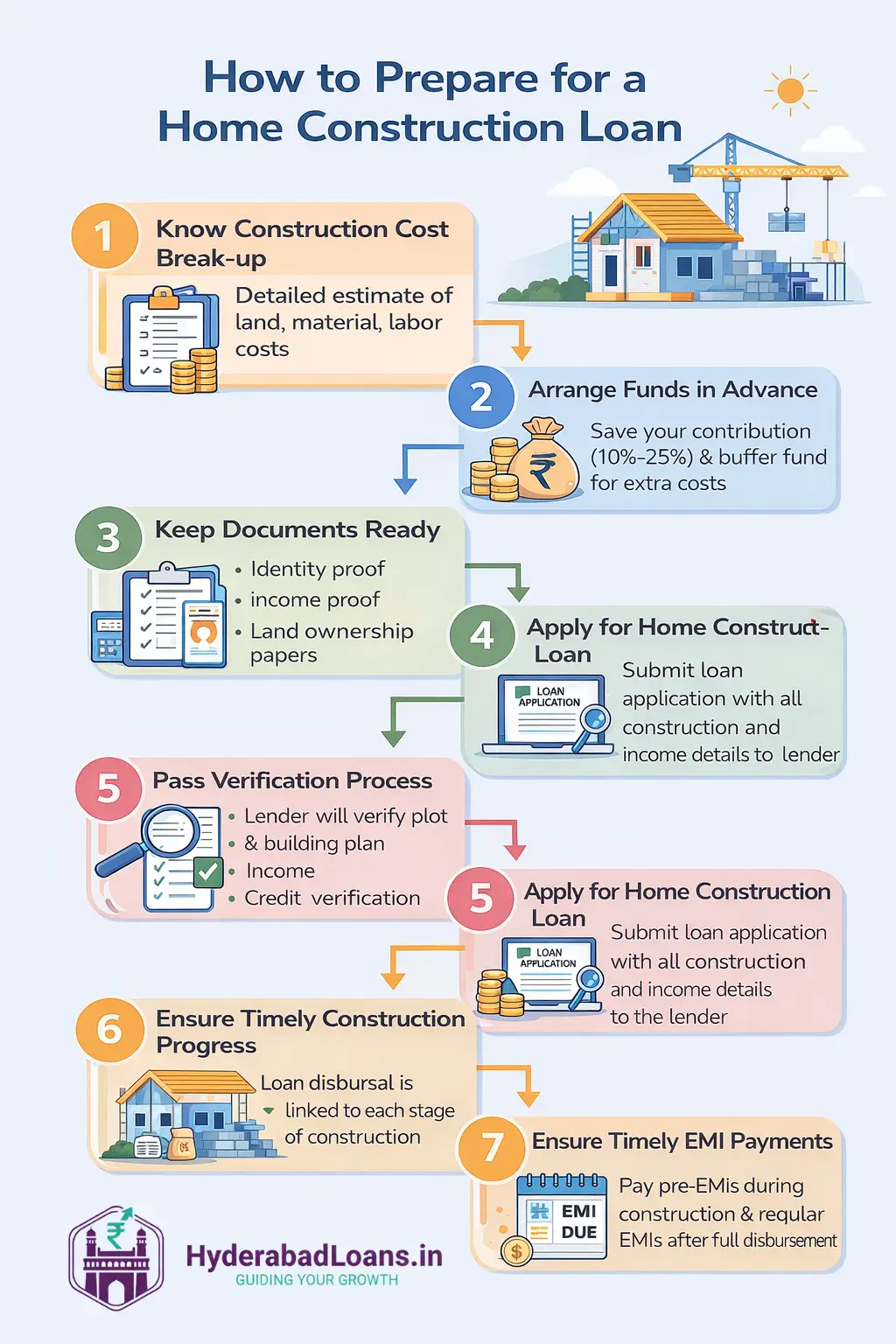

A home construction loan is a type of secured housing loan offered to individuals who own a vacant residential plot and want to construct a house on it. This loan helps cover construction-related expenses such as planning, material procurement, labour costs, and execution in a structured manner.

Unlike a regular home loan, a home construction loan is usually disbursed in stages based on construction progress. Interest is charged only on the amount disbursed, which helps reduce the initial EMI burden during the construction phase.

What Is a Home Construction Loan?

A home construction loan is designed specifically for building a residential property on land already owned by the borrower. The loan amount is sanctioned based on the approved construction estimate, borrower’s income, credit score, and repayment capacity.

Key characteristics:

- Secured against land and proposed construction

- Stage-wise fund disbursement

- Lower interest compared to unsecured loans

- Long repayment tenure

Home Construction Loan in India

In India, home construction loans are offered by:

- Public sector banks

- Private banks

- Housing finance companies and NBFCs

Most lenders finance up to 75%–90% of the total construction cost. Loan tenure can extend up to 30–32 years, depending on borrower age and profile.

Features and Benefits of Home Construction Loan

Ample Loan Amount

Borrowers can avail a sizable loan based on construction cost and income, ensuring uninterrupted progress of construction.

Flexible Tenure Options

Repayment tenure can go up to 30–32 years, helping keep EMIs affordable.

Quick Approval and Disbursement

With digital verification and streamlined processes, loan approvals and disbursements are faster compared to earlier years.

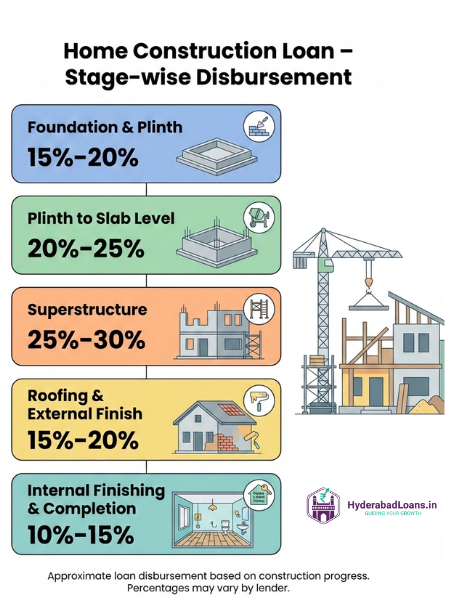

Stage-Wise Disbursement

Funds are released as per construction milestones, ensuring better financial discipline and reduced interest outgo.

Top-Up and Refinancing Facility

Borrowers may refinance existing loans or avail top-up loans to meet additional construction or finishing costs.

Tax Benefits

Tax benefits are available under applicable sections of the Income Tax Act after construction completion.

Home Construction Loan EMI Calculator – Tenure Comparison

| Loan Amount | Tenure | Interest Rate | Approx EMI |

|---|---|---|---|

| ₹50 Lakhs | 15 Years | 9% | ₹50,716 |

| ₹50 Lakhs | 20 Years | 9% | ₹44,986 |

| ₹50 Lakhs | 25 Years | 9% | ₹41,964 |

Home Construction Loan Rate of Interest

Interest rates for home construction loans in India are similar to home loan rates and depend on borrower profile and lender type.

| Lender Type | Interest Rate (p.a.) |

|---|---|

| Public Sector Banks | 8.50% – 9.75% |

| Private Banks | 8.75% – 10.50% |

| NBFCs | 9.50% – 13.00% |

Factors affecting interest rate:

- CIBIL score (750+ preferred)

- Employment type

- Loan tenure

- Construction approvals

Home Construction Loan Eligibility

Basic Eligibility Criteria

- Indian resident

- Age: 21–65 years (salaried), up to 70 years (self-employed)

- Ownership of a residential plot

- Approved building plan

- Stable income source

- CIBIL score of 700+

Income-Based Loan Eligibility (Indicative)

- ₹50,000 monthly income → ₹30–35 lakhs

- ₹1,00,000 monthly income → ₹60–70 lakhs

- ₹2,00,000 monthly income → ₹1–1.2 crore