Table of Contents

ToggleHome Loan Eligibility & EMI Planning

Home loan eligibility is assessed based on multiple factors, including monthly income, age, employment stability, credit score, existing financial obligations, and the value of the property being purchased.

Most lenders consider applicants aged between 21 and 65 years, with loan tenure extending up to 20–30 years depending on repayment capacity. Proper EMI planning helps borrowers balance monthly cash flow with long-term financial goals using tools such as the EMI calculator.

Home Loan EMI Calculator

Monthly EMI: ₹0

Total Interest: ₹0

Total Payment: ₹0

Home Loan Eligibility & EMI Planning

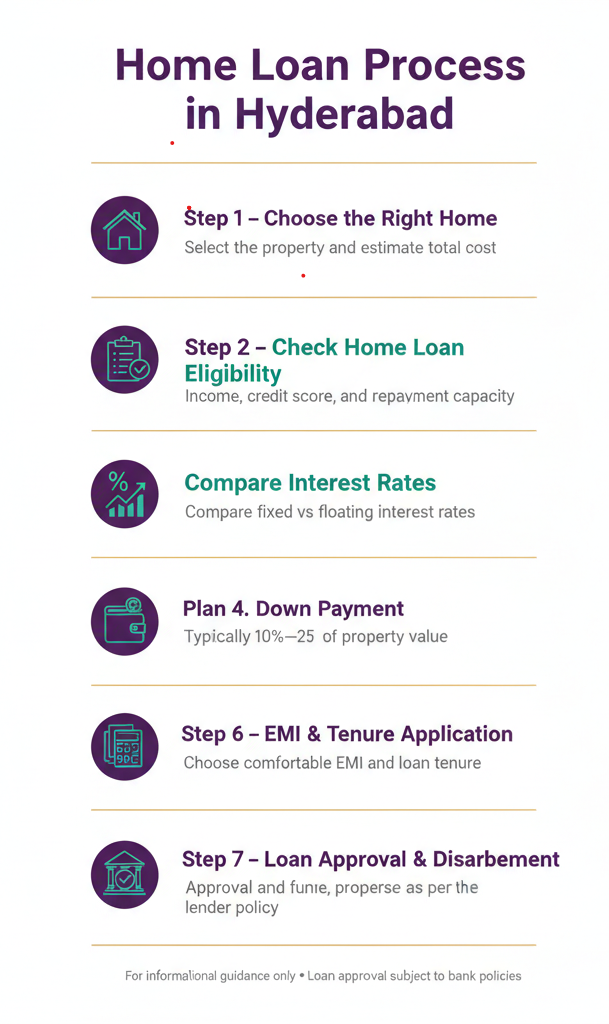

Home loan eligibility is assessed based on multiple factors, including monthly income, age, employment stability, credit score, existing financial obligations, and the value of the property being purchased. Most lenders consider applicants aged between 21 and 65 years, with loan tenure extending up to 20–30 years depending on repayment capacity. Proper EMI planning helps borrowers balance monthly cash flow with long-term financial goals.Down Payment Requirements

Most banks and housing finance companies require borrowers to contribute a portion of the property value as a down payment. In general, down payment ranges between 10% and 25% of the total property cost. Higher down payment reduces loan amount and overall interest burden.Loan Amount & Property Value Ratio

Home loan amounts are typically offered up to 75%–90% of the property value, depending on lender policies and property cost. Properties with higher market value may receive lower loan-to-value ratios.Documents Required for Home Loans

Basic Documents Required for All Applicants

- Completed application form

- Recent passport-size photographs duly signed

- Bank account details (salary or primary operating account)

- Property documents including sale agreement and approved layout or sanction map

Identity, Address & Age Proof

- Proof of Identity: PAN Card, Aadhaar Card, Passport, Driving License, or Voter ID

- Proof of Address: Aadhaar Card, Passport, Driving License, Voter ID, or utility bill

- Proof of Age: PAN Card, Aadhaar Card, Passport, or Driving License

- Signature Proof: PAN Card or Passport

Income Documents for Salaried Applicants

- Last 3 months’ salary slips

- Last 6 months’ bank statements showing salary credit

- Latest filed Income Tax Return (ITR) (usually last 1 year)

- Employment proof such as company ID card or appointment letter

Income Documents for Self-Employed Applicants

- Last 3 years’ Income Tax Returns (ITR)

- Audited balance sheet and profit & loss statement for the last 3 years

- Business existence proof such as GST registration, trade license, or incorporation documents

- Last 6–12 months’ bank statements of business accounts

Additional Supporting Documents (If Applicable)

- Educational qualification proof (for professionals)

- Relationship proof (for co-applicants)

- Property valuation and legal documents as required by the lender

How Home Loan Interest Rates Are Determined

Credit Score

Applicants with a credit score of 750 and above generally receive lower interest rates. Credit score can influence nearly 30%–40% of interest rate determination.Income & Employment Stability

Salaried applicants with stable income often receive more favorable rates than self-employed borrowers.Loan Amount & Tenure

Higher loan amounts and longer tenure may attract slightly higher interest rates.Property Type & Location

Approved residential projects in Hyderabad generally receive better financing terms.Home Loan Processing Timeline

Home loan eligibility review and processing usually takes 5 to 10 working days after submission of complete documents. Final approval and disbursement timelines depend on property verification and lender-specific procedures.

Submit Home Loan Details for Eligibility Guidance

Users can submit their basic home loan requirements through the loan information form on this page. Based on the details shared, eligibility guidance and next steps are provided before approaching banks or housing finance companies.

This page provides home loan information and guidance only. Loan approval and disbursal are subject to bank or housing finance company policies and applicant eligibility.

Home Loan Interest Rates in Hyderabad (2025–2026)

Home loan interest rates in Hyderabad typically range between 7.35% and 11.5% per annum, depending on lender policy, credit score, employment type, and loan amount. Borrowers with stronger credit profiles often receive rates closer to the lower end of this range. In addition to traditional home loan options, many lenders in the city also offer mudra loan options in Hyderabad, which cater to small businesses and entrepreneurs. These loans can provide flexible financing solutions, making it easier for potential homeowners to invest in property. Understanding the various loan products available can help borrowers make informed decisions tailored to their financial needs.

Most banks and housing finance companies require borrowers

to contribute a portion of the property value as a down payment.

In general, down payment ranges between

10% and 25% of the total property cost.

Higher down payment reduces loan amount

and overall interest burden.

Home Loan Interest Rates Public and Private banks (2025–2026)

| Bank / Lender | Type | Interest Rate (p.a.)* | Remarks |

|---|---|---|---|

| Central Bank of India | Public Sector Bank | ~7.35% onwards | Rates linked to credit score and loan scheme |

| Canara Bank | Public Sector Bank | ~7.40% onwards | Lower rates for high CIBIL score borrowers |

| Union Bank of India | Public Sector Bank | ~7.45% onwards | Interest linked to applicant profile |

| Bank of Baroda | Public Sector Bank | ~7.45% onwards | Scheme-based rates, may vary by loan amount |

| State Bank of India (SBI) | Public Sector Bank | ~7.50% onwards | Rates linked to CIBIL score and employment type |

| HDFC Bank | Private Bank | ~7.90% onwards | Faster processing, flexible tenure options |

| Kotak Mahindra Bank | Private Bank | ~7.70% onwards | Rates depend on property type and borrower profile |

| ICICI Bank | Private Bank | ~8.75% onwards | Digital application and quicker approvals |

| Axis Bank | Private Bank | ~8.75% onwards | Rates vary based on income and credit score |

| Bajaj Housing Finance | Housing Finance Company (HFC) | ~7.45% onwards | Flexible eligibility norms |

| LIC Housing Finance | Housing Finance Company (HFC) | ~8.40% onwards | Popular for long tenure loans |

| Tata Capital Housing Finance | Housing Finance Company (HFC) | ~8.75% onwards | Suitable for self-employed applicants |

*Interest rates are indicative and subject to change based on credit score, income, loan amount, tenure, and lender policies.

What is the average home loan interest rate in Hyderabad?

How much home loan can I get based on my income?

What credit score is considered good for home loan approval?

How much down payment is usually required?

Is zero down payment home loan available in Hyderabad?

In most cases, zero down payment home loans are not offered by banks or housing finance companies in India. RBI guidelines generally require borrowers to contribute a minimum 10%–25% of the property value as down payment.

How to Change my Photo from Admin Dashboard?

What is the maximum loan-to-value (LTV) ratio for home loans?

Home loan LTV ratios generally range between 75% and 90% of the property value. Lower-priced properties usually qualify for higher LTV, while premium properties may receive lower LTV limits.

What is the typical tenure offered for home loans?

Home loan tenure usually ranges from 20 to 30 years. Longer tenure reduces monthly EMI but increases total interest paid, while shorter tenure lowers total interest cost.

How long does home loan approval usually take?

Initial eligibility assessment is often completed within 2–3 working days. Complete approval and disbursement typically take 5–10 working days, subject to document verification and property legal checks.

What percentage of home loan applications get rejected?

Industry data indicates that approximately 15%–25% of home loan applications face rejection, commonly due to low credit score, high existing debt, or incomplete property documentation.

Do you approve or disburse home loans?

No. HyderabadLoans.in provides home loan information and eligibility guidance only. Loan approval and disbursement are handled by banks or housing finance companies based on their internal policies and applicant eligibility. In addition to home loans, individuals looking for financial support can also explore personal loan options in Hyderabad. These loans typically offer quick approval processes and flexible repayment terms to meet various financial needs. It is advisable to compare different lenders to find the best rates and terms that suit your requirements.

What is the current SBI home loan interest rate?

SBI home loan interest rates generally start from around 7.50% per annum for borrowers with high credit scores. The final rate depends on CIBIL score, loan amount, employment type, and SBI’s internal lending policy.

Does SBI offer lower interest rates for high CIBIL scores?

Yes. SBI follows a CIBIL-linked pricing model. Borrowers with a credit score of 750 or above are usually offered lower interest rates compared to borrowers with lower credit scores.