An EMI bounce can happen to anyone—due to a salary delay, unexpected expenses, or even a technical banking issue. While a single missed EMI may not immediately derail your finances, the actions you take after an EMI bounce play a decisive role in determining its long-term impact on your credit profile and loan eligibility.

An EMI bounce can happen to anyone—due to a salary delay, unexpected expenses, or even a technical banking issue. While a single missed EMI may not immediately derail your finances, the actions you take after an EMI bounce play a decisive role in determining its long-term impact on your credit profile and loan eligibility.

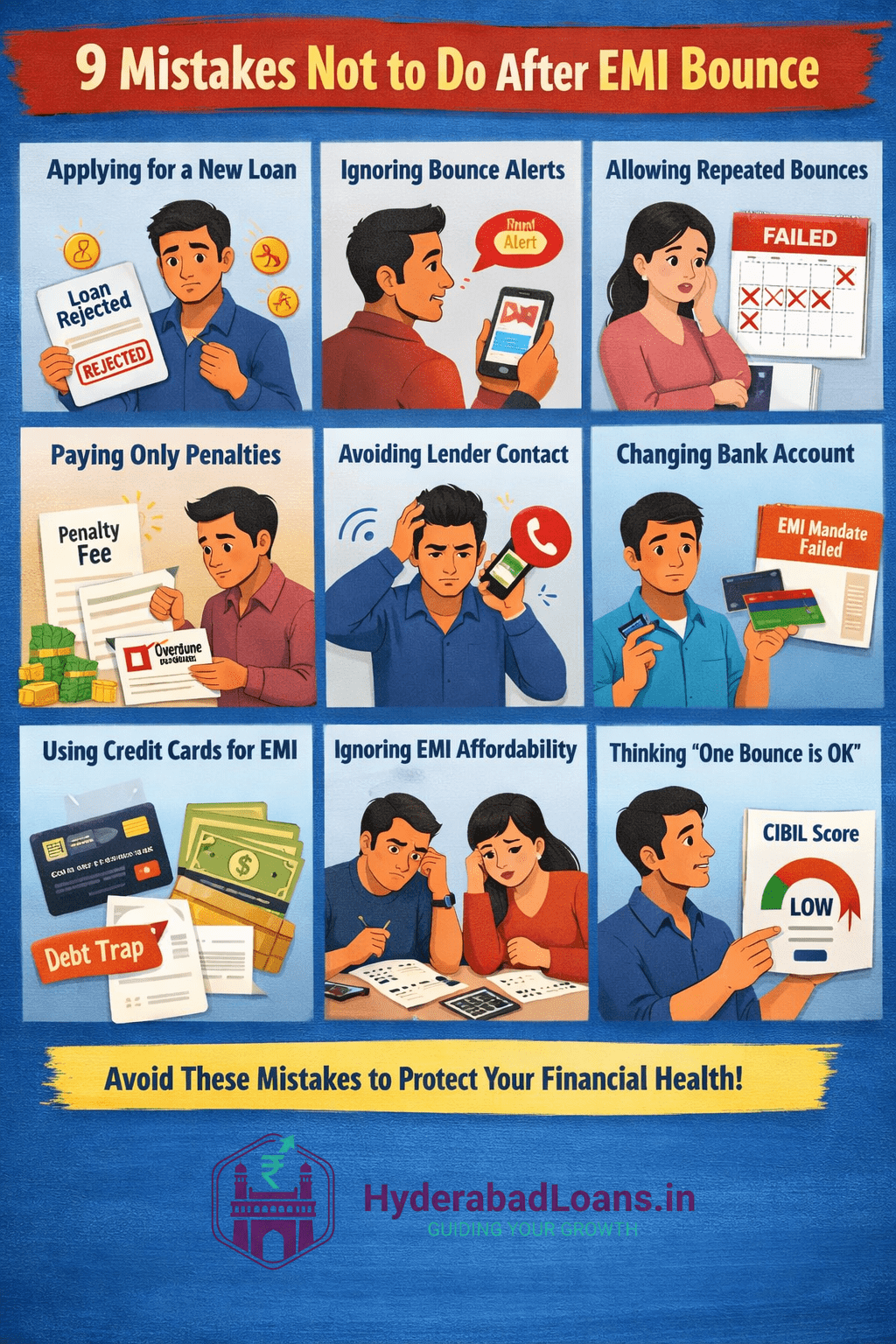

Many borrowers make avoidable mistakes after an EMI bounce that worsen the situation instead of resolving it. This article explains the 9 most common mistakes you must avoid after an EMI bounce, so you can protect your credit score and regain financial stability.

1. Applying for a New Loan Immediately After EMI Bounce

Panic often leads borrowers to apply for a fresh loan to arrange funds quickly. This is one of the most damaging steps you can take.

Why this hurts your profile

Every loan application creates a hard enquiry

EMI bounce combined with new enquiries signals repayment stress

Banks and NBFCs usually reject such applications outright

Applying for multiple loans in a short span can significantly worsen your creditworthiness. It is always better to stabilise existing repayments first instead of seeking new credit. Before applying again, borrowers should review their eligibility using tools like

loan eligibility check.

2. Ignoring EMI Bounce Alerts and Notifications

Some borrowers assume that if they ignore the message, the problem will resolve itself in the next cycle. Unfortunately, that rarely happens.

What actually happens

The EMI remains overdue

Additional charges may apply

Delays may still be reported to credit bureaus

Ignoring alerts allows the issue to grow silently and increases future complications.

3. Allowing Multiple EMI Bounces

While lenders may overlook a one-time issue, repeated EMI bounces are treated seriously.

How lenders view repeated failures

Indication of unstable cash flow

Higher probability of default

Reduced trust in borrower discipline

Multiple EMI bounces can severely affect approval chances for products like

personal loans, home loans, or business loans.

4. Paying Only EMI Bounce Charges Instead of EMI

A common misconception is that clearing bounce penalties alone fixes the issue.

Why this is a mistake

The EMI amount is still unpaid

Loan account remains overdue

Credit behaviour may still be marked as delayed

Bounce charges are only penalties. The EMI itself must be cleared to regularise the account.

5. Avoiding Communication With the Lender

Some borrowers stop answering calls or emails due to fear or embarrassment. This approach often backfires.

Why communication matters

Early discussion can prevent escalation

Lenders may offer short-term flexibility based on policy

Silence increases chances of recovery follow-ups

As per fair lending practices guided by the Reserve Bank of India, proactive borrower communication helps resolve repayment issues more smoothly.

6. Changing Bank Account Without Updating EMI Mandate

Closing or switching the bank account linked to your EMI without updating ECS/NACH details can cause repeated failures.

Common scenarios

Job change with new salary account

Closing an old savings account

Switching banks for better services

Mandate updates should always be completed formally with the lender to avoid future bounces.

7. Using Credit Cards or Informal Borrowing to Pay EMI

Using credit cards, payday apps, or informal loans to cover EMIs may offer short-term relief but creates long-term risk.

Hidden consequences

Higher interest burden

Multiple repayment commitments

Increased chances of another EMI bounce

This often converts a temporary issue into a long-term debt cycle.

8. Not Reviewing EMI Affordability After the Bounce

An EMI bounce is often a warning sign that your EMI may be stretching your budget.

What borrowers should reassess

Monthly income vs total EMIs

Rising household expenses

Availability of emergency savings

Using an

EMI calculator can help reassess affordability and prevent future repayment stress.

9. Assuming One EMI Bounce Has No Long-Term Impact

Many borrowers believe a single EMI bounce does not matter. This assumption can be risky.

Reality check

Even one delayed payment may appear in credit records

Lenders evaluate overall repayment behaviour, not isolated events

Impact may surface during future loan applications

While recovery is possible, careless behaviour after the bounce can slow down credit score improvement.

Quick Summary: 9 Mistakes Not to Do After EMI Bounce

| Mistake | Why It’s Risky |

|---|---|

| Applying for new loans | High rejection & credit damage |

| Ignoring bounce alerts | Penalties and reporting risk |

| Repeated EMI failures | Severe impact on credit score |

| Paying only penalties | EMI still overdue |

| Avoiding lender calls | Escalation risk |

| Changing bank account casually | Mandate failures |

| Using credit cards to pay EMI | Debt trap risk |

| Ignoring affordability review | Future defaults likely |

| Assuming one bounce doesn’t matter | Hidden long-term impact |

Final Takeaway

An EMI bounce is a temporary setback, but the mistakes made after it can have lasting consequences. Avoiding these 9 actions helps protect your credit score, maintain lender trust, and improve long-term loan eligibility.

Timely corrective steps, disciplined repayment behaviour, and calm decision-making are the keys to recovering smoothly after an EMI bounce.