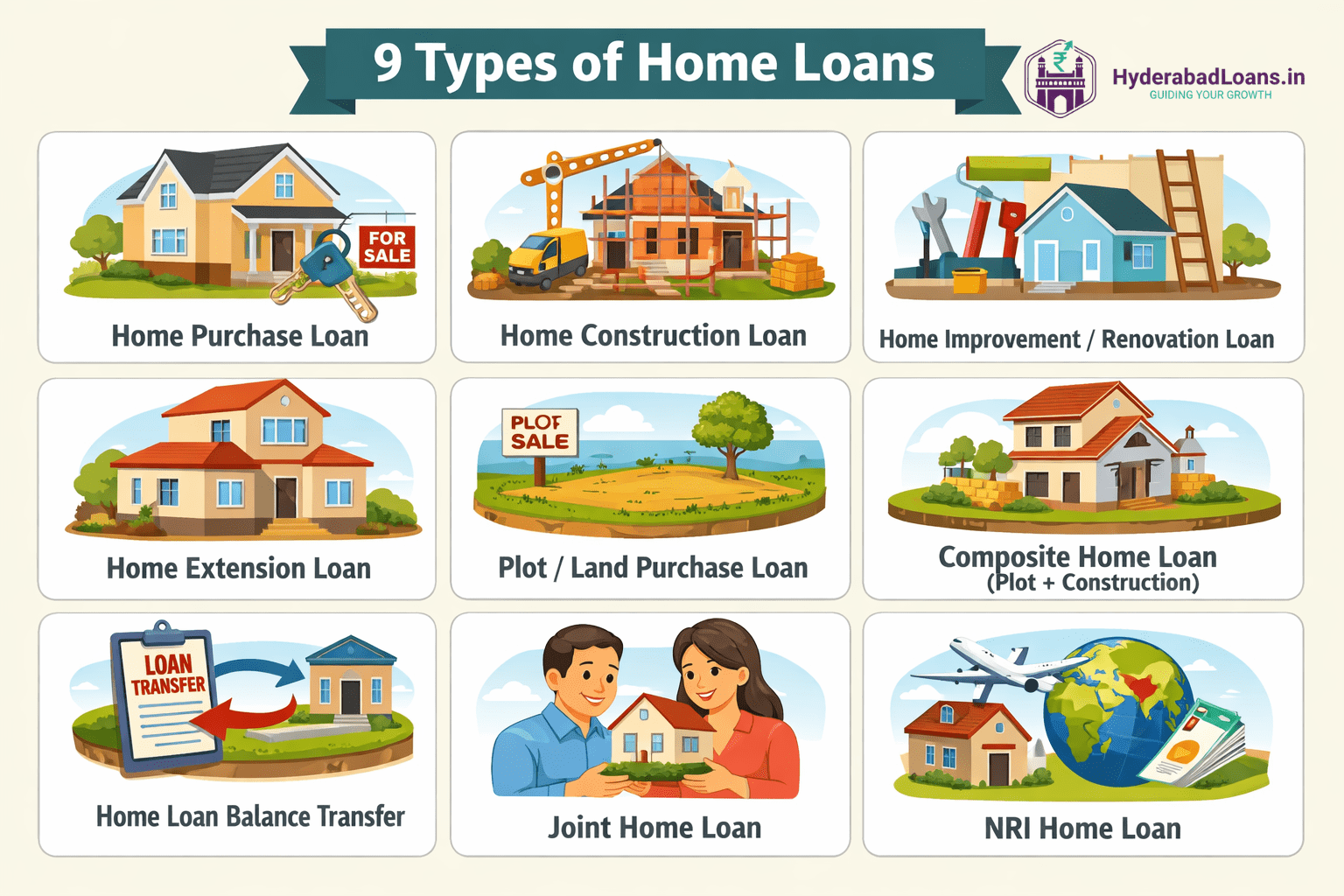

Types of Home Loans in India – Complete Guide for Home Buyers

Buying or building a home is one of the most important financial milestones for Indian families. With rising property prices and long repayment horizons, choosing the right type of home loan becomes just as important as selecting the property itself. Banks and NBFCs in India offer multiple home loan variants, each designed for a specific housing purpose and borrower profile.

This guide explains the types of home loans in India, their features, eligibility context, and who each loan is best suited for—helping you make an informed, RBI-compliant decision.

1. Home Purchase Loan

A Home Purchase Loan is the most common home loan option. It is used to buy a ready-to-move-in or under-construction residential property.

Key Features

- Used for purchasing new or resale houses/flats

- Financing typically up to 75%–90% of the property value (subject to lender policy)

- Loan tenure can extend up to 30 years

- Interest rates are generally lower compared to unsecured loans

Best Suited For

- First-time home buyers

- Salaried or self-employed individuals buying apartments or independent houses

For city-specific eligibility and documentation, many borrowers refer to detailed guides on home loans in Hyderabad to understand local lending norms.

2. Home Construction Loan

A Home Construction Loan is taken when you already own a residential plot and want to construct a house on it.

Key Features

- Loan is disbursed in stages based on construction progress

- Interest is charged only on the disbursed amount (Pre-EMI option available)

- Approved construction plan and cost estimate are mandatory

- Interest rates are similar to regular home loans

Best Suited For

- Individuals constructing independent homes

- Plot owners planning self-construction

You can explore construction-stage funding details on the home construction loan page for better clarity.

3. Home Improvement / Renovation Loan

A Home Improvement Loan is used to renovate, repair, or upgrade an existing residential property.

Key Features

- Covers painting, flooring, plumbing, electrical work, and structural repairs

- Lower loan amount compared to purchase loans

- Shorter tenure, usually up to 10–15 years

- Faster processing due to smaller ticket size

Best Suited For

- Homeowners upgrading older properties

- Renovation before renting or resale

4. Home Extension Loan

A Home Extension Loan is taken to add new space to an existing house, such as an additional room, floor, or balcony.

Key Features

- Requires approved building and extension plans

- Proof of property ownership is mandatory

- Interest rates are similar to standard home loans

- Tax benefits may apply, subject to conditions

Best Suited For

- Growing families needing more living space

- Homeowners adding extra floors or rooms

5. Plot / Land Purchase Loan

A Plot Loan is used to purchase residential land for future construction.

Key Features

- Lower loan-to-value ratio, usually 50%–70%

- Interest rates slightly higher than regular home loans

- Construction is often required within a defined time period

- Limited tax benefits until construction begins

Best Suited For

- Buyers investing in residential plots

- Long-term home construction planning

6. Composite Home Loan

A Composite Home Loan combines plot purchase and construction financing into a single loan.

Key Features

- One loan for land purchase and house construction

- Construction must begin within the lender’s specified timeline

- Stage-wise disbursement for construction

- Simplified repayment under a single account

Best Suited For

- Borrowers buying land and building immediately

7. Home Loan Balance Transfer

A Home Loan Balance Transfer allows you to shift your existing home loan to another lender offering better terms.

Key Features

- Potentially lower interest rates

- Reduced EMI or shorter loan tenure

- Option to avail a top-up loan (subject to eligibility)

Best Suited For

- Borrowers paying higher interest rates

- Those looking to improve monthly cash flow

You can understand refinancing scenarios in detail on the loan balance transfer guide.

8. Joint Home Loan

A Joint Home Loan is taken with a co-applicant, commonly a spouse or parent.

Key Features

- Higher combined loan eligibility

- Shared repayment responsibility

- Tax benefits can be claimed individually, subject to ownership

Best Suited For

- Couples or families purchasing property together

9. NRI Home Loan

An NRI Home Loan is designed for Non-Resident Indians purchasing residential property in India.

Key Features

- Income assessed in foreign currency

- Power of Attorney usually required

- Interest rates may be slightly higher

- Property must be residential

Best Suited For

- NRIs investing or planning to settle in India

Comparison Table: Types of Home Loans in India

| Home Loan Type | Purpose | Tenure | Interest Level* |

|---|---|---|---|

| Home Purchase Loan | Buy new/resale home | Up to 30 years | Low |

| Construction Loan | Build on owned plot | Up to 30 years | Low |

| Improvement Loan | Renovation/repair | Up to 15 years | Medium |

| Extension Loan | Add rooms/floors | Up to 20 years | Low |

| Plot Loan | Buy residential land | Up to 15 years | Medium |

| Composite Loan | Plot + construction | Up to 30 years | Low |

| Balance Transfer | Shift existing loan | Remaining tenure | Lower |

*Interest levels are indicative and subject to lender eligibility, credit profile, and market conditions.

How to Choose the Right Home Loan?

Before finalising a home loan, consider:

- Purpose of the loan

- Fixed vs floating interest rate preference

- Loan tenure and EMI affordability

- Tax benefits applicability

- Disbursement structure

- Long-term income stability

Many borrowers also use tools like an EMI calculator to assess monthly repayment comfort before applying.

FAQs on Types of Home Loans

Which type of home loan is best for first-time buyers?

Home purchase loans are generally suitable for first-time buyers due to longer tenures and relatively lower interest rates.

Is a plot loan considered a home loan?

Plot loans are classified separately and usually carry slightly higher interest rates and lower tax benefits until construction starts.

Can I switch my home loan later?

Yes, borrowers may opt for a balance transfer if better terms are available, subject to lender approval.

Final Thoughts

Understanding the different types of home loans helps you align borrowing with your housing goals and financial capacity. Whether you are buying, building, renovating, or refinancing, selecting the right home loan structure can significantly reduce long-term costs. Always evaluate terms carefully, as per guidelines issued by the Reserve Bank of India, and remember that interest rates and eligibility are subject to lender policies and your credit profile.

Suggested External References

- Reserve Bank of India – Housing Loan & Credit Guidelines

- Government of India – Financial Consumer Education Resources