What Are the Film Funding Options in India?

What Are the Film Funding Options in India?

Film funding is one of the biggest challenges for filmmakers in India. Many people believe that films are funded based only on scripts, star cast, or creative ideas. In reality, film funding in India works mainly on financial strength, assets, income stability, and repayment ability. This post explains the different film funding options available in India, how each option works, and which type of filmmaker each option is suitable for. For an overall understanding of structured film funding in India, it helps to first understand how lenders evaluate risk.

Understanding Film Funding in India

Film funding refers to arranging money for film-related expenses such as pre-production, shooting, post-production, marketing, and distribution. In India, banks and NBFCs treat film funding as business financing, not speculative or creative financing. Because film revenues are unpredictable, lenders focus more on risk control. That is why collateral-backed and income-backed funding options are more common than idea-based funding.

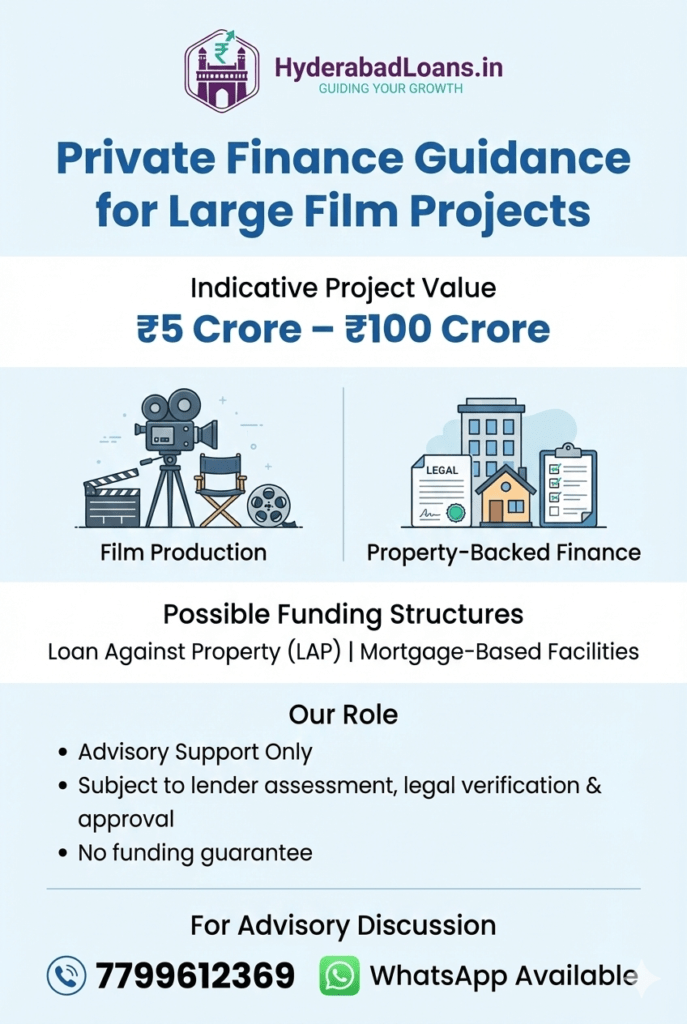

Mortgage-Based Film Funding (Most Common Option)

Mortgage-based funding is the most commonly used and reliable film funding option in India. This method involves taking a loan against residential or commercial property and using the funds for film production. In lending terms, this works similarly to a loan against property used for large business purposes.

How Mortgage-Based Film Funding Works

In mortgage-based film funding, the borrower pledges a residential, commercial, or land property as security to the lender. Based on the property’s market value, the lender sanctions a loan amount. The sanctioned amount depends largely on the type of property being mortgaged.

For open land, lenders usually offer a lower Loan-to-Value (LTV) because land carries higher resale and liquidity risk. Typically, funding ranges between 40% and 50% of the property value.

For example, if an open land parcel is valued at ₹100 crore, the eligible loan amount may range between ₹40 crore and ₹50 crore, subject to location, legal clarity, and market conditions.

In the case of a constructed or completed building property, lenders are generally more comfortable and may offer a higher LTV. For such properties, funding can range between 50% and 70% of the market value.

For instance, if a building property is valued at ₹100 crore, the loan amount may range between ₹50 crore and ₹70 crore. The final eligibility depends on factors such as the building’s condition, usage, rental income (if any), borrower profile, and overall risk assessment.

All loan approvals are subject to property valuation, borrower credit profile, income stability, and lender-specific terms and conditions.

Key Features

Interest rates typically range from 10.4% to 24%+ per annum. The exact rate depends on property value, client credit profile, income stability, and project feasibility. Loan tenure generally ranges from 10 to 20 years. This option is suitable for producers, directors, actors, technicians, or individual financiers who own property.

Business Loans for Film Production

Business loans are another film funding option, mainly available to registered production houses with financial history. These loans follow the same assessment approach as standard business loans in Hyderabad.

How Business Loans Work

Lenders assess the production company’s income, bank statements, and repayment capacity. The loan is approved based on business performance, not the film idea.

Typical Loan Structure

Loan amounts usually range from ₹1 crore to ₹100 crores. Interest rates are higher compared to mortgage loans, typically between 14% and 24%+ per annum. Repayment tenure is usually 3 to 5 years. Business loans are generally not suitable for first-time filmmakers without income proof.

Private Investors and Co-Producer Funding

Private investor funding is a non-loan-based film funding option commonly used in Indian cinema.

How Private Funding Works

In this model, investors or co-producers contribute funds in exchange for profit sharing, rights, or revenue participation.

Pros and Cons

The advantage is that there is no fixed EMI. However, profits must be shared, and creative control may be diluted. Since this option is not regulated, legal agreements must be very clear.

Distributor Advance or Minimum Guarantee (MG)

Distributors sometimes provide advances to producers before a film’s release.

How Distributor Funding Works

The distributor pays an advance amount, which is later recovered from theatrical or non-theatrical revenues.

Limitations

This option is mostly available to experienced producers. It depends heavily on cast value, director reputation, genre demand, and market conditions.

OTT Platform Pre-Buy or Licensing

OTT platforms have become an additional funding option in recent years.

Reality of OTT Funding

OTT platforms may pre-buy digital rights or partially fund production. However, such deals are highly selective and usually limited to known producers or creators with proven success. OTT funding should not be considered a guaranteed or primary funding option.

Government Film Grants and Subsidies

Some state governments India offer grants or subsidies to promote regional cinema and cultural storytelling.

Nature of Government Support

Support is usually provided as shooting subsidies, tax rebates, or reimbursement of eligible expenses.

Key Limitations

Most government benefits are reimbursements given after project completion. Approval processes are slow and documentation-heavy.

Hybrid Film Funding Model

Many filmmakers use a hybrid model by combining personal savings with loans.

Why the Hybrid Model Works

This approach reduces total borrowing, lowers EMI burden, and offers better financial control. It is commonly used for mid-budget films.

Film Funding Examples for Big-Budget Projects in India

Big-budget film projects in India require careful financial planning because the risk and capital involved are much higher. For such projects, funding is usually arranged through a combination of mortgage loans, business loans, and industry partnerships rather than a single source.

Example 1: Big-Budget Commercial Film Using Mortgage Funding

A producer plans a commercial film with a total budget of ₹20 crore. The producer owns a commercial property valued at ₹12 crore. Based on a typical Loan-to-Value ratio of around 50%, the lender approves a mortgage loan of approximately ₹6 crore. The loan is taken for a tenure of 15 years. The remaining budget is arranged through advances, personal capital, or staggered payments during production. This structure helps the producer manage cash flow while keeping EMIs relatively stable. Producers often estimate repayments using an EMI calculator before finalising the loan.

Example 2: Big Production House Using Business Loan + Internal Funds

An established production house plans a ₹15 crore film and has a strong income history from previous projects. The production house raises ₹5 crore through internal funds and applies for a business loan of ₹4 crore based on its financial statements and banking history. The loan is approved for a tenure of 5 years at a higher interest rate compared to mortgage funding. The balance amount is managed through pre-sales, music rights, or distribution arrangements.

Example 3: Large Film with Multiple Funding Sources

A high-profile film with a budget of ₹100 crore uses a multi-layer funding approach. The main producer takes a mortgage loan of ₹50 crore against property. A co-producer contributes ₹20 crore in exchange for profit sharing. The distributor provides a minimum guarantee for specific territories, and digital rights are licensed to an OTT platform. This diversified funding structure reduces dependency on a single source and spreads financial risk.

Example 4: Big Project Backed by OTT and Distributor Advances

A well-known director with an established cast plans a ₹100 crore film. An OTT platform agrees to pre-buy digital rights, covering a significant portion of the budget about 20–30% of film. Additionally, distributors provide advances for theatrical rights in select regions 20%. The producer may still use short-term funding or a small mortgage loan to manage working capital during production.

Key Learning from Big Film Funding Examples

Large film projects in India are rarely funded through a single loan. Instead, they rely on a mix of mortgage-backed loans, business loans, private investments, distributor advances, and OTT licensing. For big-budget films, lenders focus heavily on asset strength, repayment visibility, and the producer’s financial credibility rather than creative factors alone. These principles are central to structured film funding in India.

Common Myths About Film Funding in India

There are no script-based bank loans, guaranteed film finance approvals, zero-interest film loans, or 100% funding options without collateral. Legitimate lenders do not fund films purely on creative ideas.

Key Takeaways

Film funding in India is asset-backed and income-driven. Mortgage loans form the backbone of film financing. Interest rates depend on property value, client profile, credit score, and project feasibility. Understanding these realities helps filmmakers plan funding responsibly and avoid risky decisions.

Pingback: Private Funding for Films | Investors, Rates & LAP Options