Government Doctor Loans vs Private Doctor Loans

Government Doctor Loans vs Private Doctor Loans

Doctors across India—especially in Hyderabad and Telangana—often require loans for clinic setup, medical equipment, home purchase, or personal financial needs. While lenders offer loans for doctors in India across categories, the terms can differ significantly based on whether the applicant is a government doctor or a private doctor.

This in-depth comparison of government doctor loans vs private doctor loans explains eligibility, interest rates, documentation, and practical suitability—using RBI-compliant, non-promissory language to help doctors make informed decisions.

Overview: Doctor Loan Categories in India

Doctor loans are professional loans designed considering the income stability and long-term earning potential of medical professionals. These may be structured as:

Personal loans

Business/clinic loans

Loan Against Property (LAP)

The employment nature—government service vs private practice—plays a major role in how lenders assess risk, pricing, and tenure.

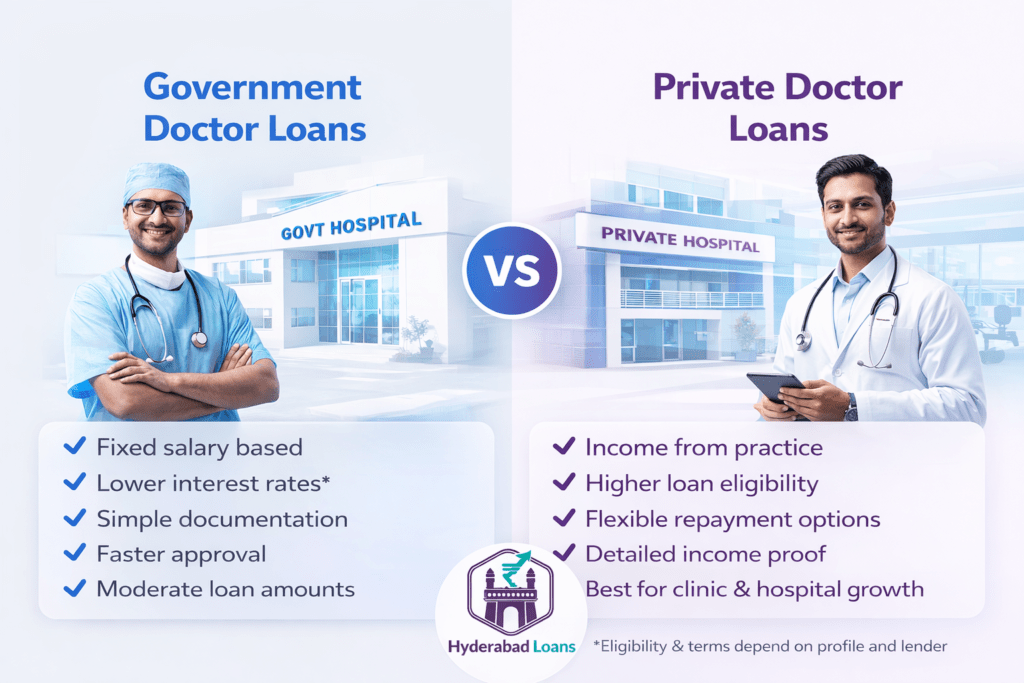

What Are Government Doctor Loans?

Government doctor loans are offered to doctors employed with:

Central or State Government hospitals

Government medical colleges

Public sector healthcare institutions

Autonomous bodies under government control

These doctors typically receive fixed monthly salaries via official payroll systems, which lenders consider highly stable.

Government Doctor Loan Benefits

Common government doctor loan benefits include:

Lower perceived credit risk due to permanent employment

Predictable monthly income for EMI assessment

Longer repayment tenures, especially for home loans

Simplified income verification through salary slips

Note: Final approval and pricing depend on credit score, age, and lender policy.

What Are Private Doctor Loans?

Private doctor loans are designed for doctors who are:

Running private clinics or hospitals

Working in private hospitals

Self-employed consultants or specialists

Visiting or part-time practitioners

Since income may vary, lenders rely more heavily on financial records and practice performance.

Private Doctor Loan Eligibility

Private doctor loan eligibility is commonly assessed using:

Years of professional practice (usually 2–3 years+)

Average monthly or annual income

Income Tax Returns (ITR)

Clinic or hospital revenue (if applicable)

Banking history and CIBIL score

Private doctors often qualify for higher loan amounts, especially for business-related funding.

Eligibility Comparison: Government vs Private Doctor Loans

| Parameter | Government Doctor | Private Doctor |

|---|---|---|

| Employment Type | Permanent government service | Self-employed / private hospital |

| Minimum Experience | 1–2 years | 2–3 years |

| Income Proof | Salary slips | ITR & bank statements |

| Income Stability | Very high | Moderate to high |

| Credit Score Weightage | Medium | High |

Interest Rate Comparison

Interest rates are indicative and may vary by lender, credit profile, and market conditions.

| Loan Type | Government Doctor Loans | Private Doctor Loans |

|---|---|---|

| Personal Loan | ~9% – 12% p.a. | ~11% – 18% p.a. |

| Home Loan | ~7.5% – 10% p.a. | ~8.75% – 10.5% p.a. |

| Business / Clinic Loan | Limited availability | ~11.5% – 18% p.a. |

Documents Required: Government vs Private Doctors

| Document | Government Doctor | Private Doctor |

|---|---|---|

| PAN & Aadhaar | Required | Required |

| Medical Degree & Registration | Required | Required |

| Income Proof | Salary slips | ITR (2–3 years) |

| Bank Statements | Last 6 months | 6–12 months |

| Clinic Registration | Not applicable | Required (if applicable) |

Loan Features Comparison

| Feature | Government Doctor Loans | Private Doctor Loans |

|---|---|---|

| Ease of Approval | High | Moderate |

| Maximum Tenure | Up to 30 years (home loans) | Up to 20–25 years |

| Loan Amount Flexibility | Moderate | High (income-based) |

| Business Funding Options | Limited | Extensive |

Which Doctor Loan Option Is Right for You?

Choosing between government doctor loans vs private doctor loans depends on your professional profile:

Government doctors benefit from stability and potentially lower rates

Private doctors gain flexibility and higher eligibility for clinic expansion

Business and equipment loans are more accessible to private practitioners

There is no one-size-fits-all solution—loan suitability depends on income structure, financial goals, and repayment capacity.

Frequently Asked Questions (FAQs)

Do government doctors always get lower interest rates?

Often yes, due to stable employment. However, final rates depend on credit score and lender policy.

Can private doctors get higher loan amounts?

Yes. Doctors with established practices and strong income may qualify for higher limits.

Are business loans available for government doctors?

Usually limited, unless the doctor runs a registered private practice alongside service.

Is collateral mandatory for doctor loans?

Not for personal loans. LAP and home loans typically require collateral.

Does specialization affect eligibility?

Specialization may influence income assessment, but overall financial stability matters more.