Current Home Loan Interest Rate in 2026: Trends, Current Ranges & What Borrowers Should Know

Home loan interest rates play a crucial role in determining the overall cost of buying a house. In 2026, homebuyers and existing borrowers in India are closely tracking interest rate movements due to changing economic conditions, inflation trends, and policy decisions. Understanding how home loan interest rates work in 2026 can help borrowers plan better, choose the right loan structure, and avoid long-term financial stress.

This article explains the current home loan interest rate scenario in 2026, factors influencing rates, how lenders price loans, and what borrowers should keep in mind before applying or refinancing.

Overview of Home Loan Interest Rates in 2026

In 2026, home loan interest rates in India are largely influenced by the monetary policy stance of the Reserve Bank of India, liquidity conditions in the banking system, and lenders’ internal cost of funds. Most banks and housing finance companies are offering floating-rate home loans, with pricing linked to external benchmarks such as the repo rate.

For borrowers with strong credit profiles, stable income, and lower loan-to-value ratios, home loan interest rates are generally available at the lower end of the prevailing range. Borrowers with average credit scores or higher risk profiles may see relatively higher rates.

It is important to note that interest rates are indicative and not guaranteed, and final rates depend on individual eligibility and lender assessment.

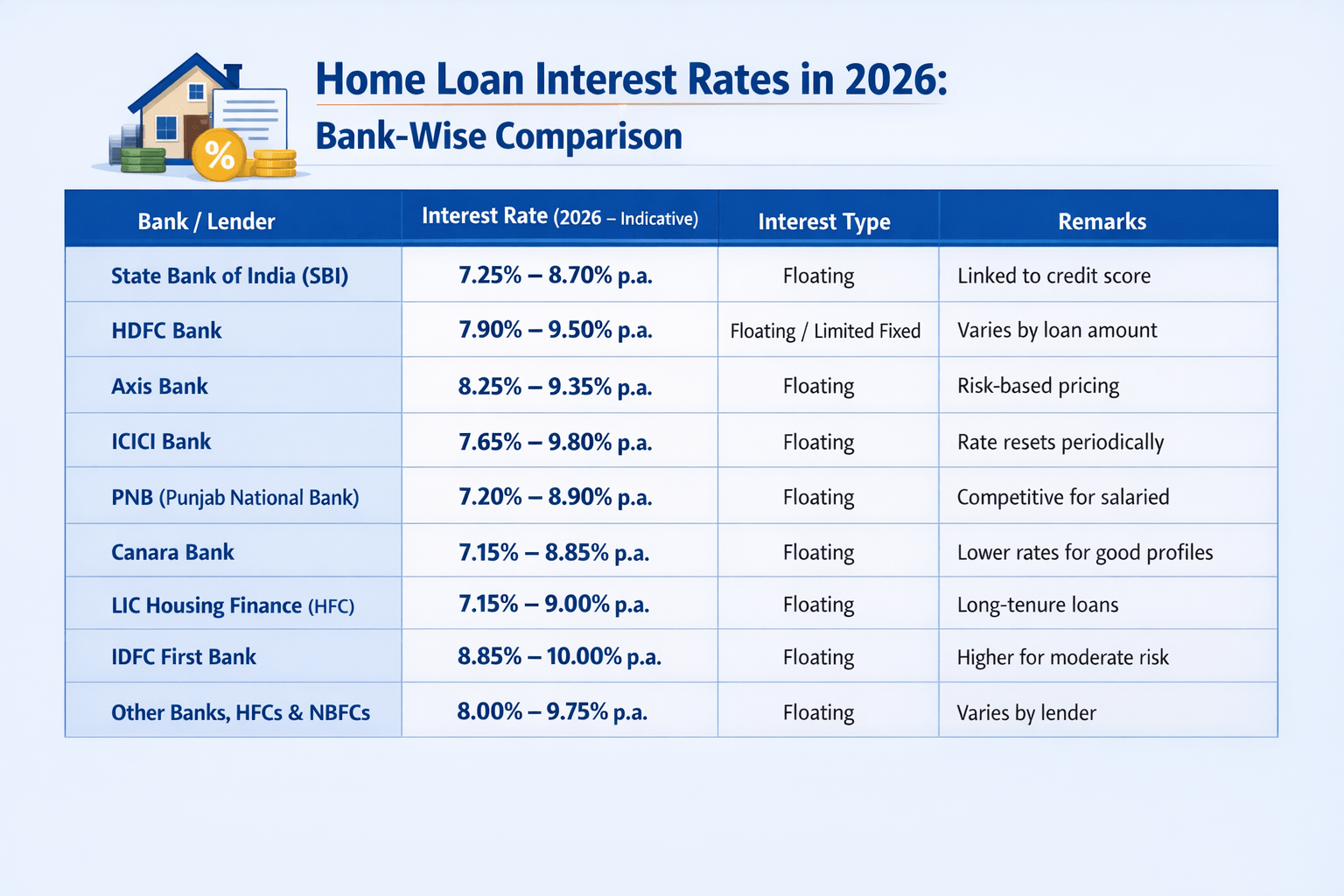

Indicative current Home Loan Interest Rate Range in India (2026)

As of 2026, the home loan interest rate environment in India broadly falls within the following range:

- Lower range: Around 7.1% – 7.5% per annum for strong credit profiles

- Mid-range: Around 7.6% – 8.5% per annum for average salaried borrowers

- Higher range: Around 8.6% – 9.5% per annum for higher-risk profiles or specific loan products

These rates may vary based on whether the borrower is salaried or self-employed, the loan amount, property type, and tenure.

Key Factors That Influence Home Loan Interest Rates in 2026

1. RBI Monetary Policy and Repo Rate

The repo rate set by the Reserve Bank of India directly impacts home loan interest rates, especially for loans linked to external benchmarks. When the repo rate changes, floating-rate home loans may be reset accordingly, depending on the lender’s reset cycle.

2. Credit Score and Repayment History

A borrower’s credit score remains one of the most critical factors in 2026. Borrowers with higher credit scores and clean repayment histories generally receive more favourable interest rates compared to those with past defaults, EMI bounces, or high credit utilisation.

3. Loan Amount and Loan-to-Value Ratio (LTV)

Lower LTV ratios, where the borrower contributes a higher down payment, often attract better interest rates. Higher loan amounts relative to property value may be priced with additional risk margins.

4. Employment Profile and Income Stability

Salaried borrowers with stable employment, especially in organised sectors, usually receive more competitive rates than self-employed borrowers with fluctuating income patterns.

5. Type of Interest Rate (Floating vs Fixed)

In 2026, floating-rate home loans are more common than fixed-rate loans. Fixed-rate options may be available for limited tenures or at higher interest rates due to interest rate risk borne by the lender.

Floating vs Fixed Home Loan Interest Rates in 2026

Floating Interest Rate

Floating rates move in line with market benchmarks. In 2026, most home loans are offered on a floating basis, which means EMIs may increase or decrease depending on rate movements.

Pros:

- Benefit from rate cuts when market rates fall

- Lower initial interest rates compared to fixed loans

Cons:

- EMIs can increase if interest rates rise

Fixed Interest Rate

Fixed-rate home loans offer stability in EMIs for a specified period.

Pros:

- Predictable EMIs for a defined duration

Cons:

- Generally higher interest rates

- Limited availability in 2026

How Home Loan Interest Rates Affect EMI and Total Cost

Even a small change in home loan interest rates can significantly affect the total repayment amount over long tenures such as 20 or 25 years. For example, a difference of 0.5% in interest rate can translate into several lakhs of rupees in additional interest over the loan tenure.

This is why borrowers are advised to:

- Choose affordable EMIs rather than maximum eligibility

- Opt for shorter tenures where feasible

- Make prepayments when surplus funds are available, subject to lender terms

Using an EMI calculator helps borrowers understand the long-term impact of interest rates before finalising a loan.

Home Loan Interest Rates for New Buyers vs Existing Borrowers

New Home Loan Applicants

In 2026, new applicants can often negotiate interest rates based on credit score, loan amount, and relationship with the bank. Comparing offers across lenders remains important, but borrowers should avoid excessive loan enquiries.

Existing Home Loan Borrowers

Existing borrowers should regularly review their interest rate and outstanding balance. If rates reduce in the market but the loan rate remains high, borrowers may consider options such as repricing requests or balance transfer, subject to eligibility and cost-benefit analysis.

Special Considerations for Homebuyers in 2026

- Women borrowers may receive small interest rate concessions from select lenders

- Affordable housing segments may have preferential pricing under specific schemes

- Property location, project approval status, and builder credibility can influence lender pricing

Borrowers should always read the loan agreement carefully to understand reset clauses, spread over benchmark, and prepayment conditions.

Common Myths About Home Loan Interest Rates

“Lowest advertised rate is guaranteed”

No. Advertised rates are indicative and subject to eligibility, credit score, and lender discretion.

“Once fixed, the rate never changes”

Even fixed-rate loans may have reset clauses after a defined period.

“Interest rate is the only cost”

Processing fees, insurance, and other charges also impact overall cost.

Final Thoughts: Planning Home Loans Smartly in 2026

Home loan interest rates in 2026 remain competitive but require careful evaluation. Rather than focusing only on the lowest rate, borrowers should consider affordability, tenure, flexibility, and long-term financial comfort.

A well-planned home loan with a manageable EMI, aligned with income stability and future goals, can make homeownership sustainable and stress-free. Staying informed about interest rate trends and reviewing loans periodically can help borrowers make smarter decisions throughout the loan tenure.