What Happens If EMI Bounces? Consequences, Charges & What to Do Next

What Happens If EMI Bounces? Consequences, Charges & What to Do Next

An EMI bounce occurs when your bank is unable to debit the scheduled loan EMI from your account due to insufficient balance or technical issues. While a single EMI bounce may seem minor, repeated failures can have serious financial and legal consequences.

This blog explains what happens if EMI bounces, how banks respond, applicable charges, impact on credit score, and practical steps you can take to avoid long-term damage.

What Is an EMI Bounce?

An EMI bounce happens when the auto-debit (ECS / NACH mandate) fails on the due date. This can occur for multiple reasons, including low account balance, mandate expiry, or bank-side issues.

From a lender’s perspective, an EMI bounce is treated as a missed payment, even if the delay is unintentional.

Common Reasons Why EMI Bounces

- Insufficient balance in the linked bank account

- Salary credit delay

- ECS / NACH mandate expiry or cancellation

- Change in bank account without updating lender

- Technical or banking system issues

Understanding the cause is important, as it determines how quickly the issue can be resolved.

What Happens If EMI Bounces?

When an EMI bounces, the consequences usually follow a structured sequence:

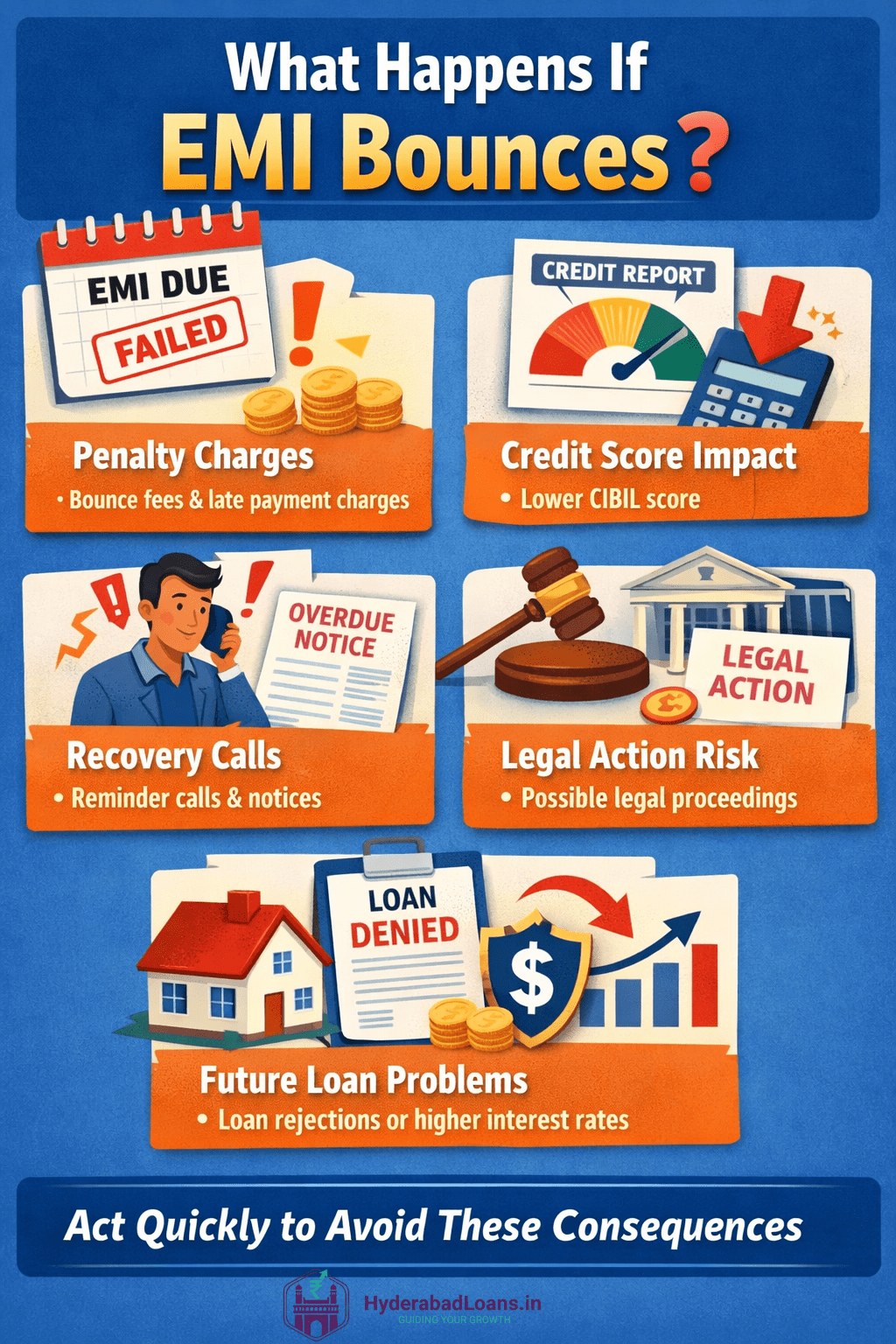

1. EMI Bounce Charges Are Applied

Most banks and NBFCs levy a fixed penalty when an EMI fails. This charge is added to your loan account and increases your outstanding amount.

2. Late Payment Fees & Penal Interest

If the EMI is not cleared within the grace period (if any), lenders may apply late payment charges or penal interest on the overdue amount.

3. Credit Score Impact

Repeated EMI bounces or delayed payments are reported to credit bureaus. Even a single missed EMI can negatively impact your CIBIL score, especially if not rectified quickly.

4. Recovery Follow-Ups

Lenders may initiate reminder calls, SMS alerts, or emails. Persistent defaults can lead to formal recovery actions, depending on loan terms.

5. Legal Action (In Severe Cases)

In rare cases of repeated defaults, lenders may initiate legal proceedings under applicable banking and contract laws. This typically happens only after multiple missed EMIs.

EMI Bounce Charges in India (Indicative)

| Type of Charge | Indicative Amount |

|---|---|

| EMI bounce penalty | ₹300 – ₹750 per bounce |

| Late payment charges | ₹500 – ₹1,000 or as per lender policy |

| Penal interest | 2% – 3% per month on overdue amount |

Note: Charges are indicative and vary by lender, loan type, and loan agreement terms.

Does EMI Bounce Affect Credit Score?

Yes. An EMI bounce can negatively impact your credit score if it is reported as a missed or delayed payment to credit bureaus. Even a single missed EMI may affect your credit profile, depending on how quickly the payment is regularised.

Key Factors That Influence Credit Score Impact

- Number of times the EMI has bounced

- Delay duration before the overdue EMI is cleared

- Your overall repayment track record

- Type of loan (secured or unsecured)

Borrowers with a strong and consistent repayment history may see only a temporary dip in their credit score. However, repeated EMI bounces or prolonged delays can lead to a noticeable decline and slower recovery.

Banks and NBFCs generally report repayment behaviour on a monthly basis, so unresolved EMI bounces can remain visible on your credit report for several months.

How EMI Bounce Affects Future Loan Eligibility

Lenders consider EMI bounces as indicators of repayment stress and cash flow mismanagement. When evaluating new loan applications, banks closely examine past EMI behaviour to assess risk.

Possible Impact on Future Loan Applications

- Lower sanctioned loan amount than requested

- Higher interest rates due to increased risk perception

- Stricter eligibility checks and documentation requirements

- Reduced chances of approval for unsecured loans

For borrowers with multiple past bounces, lenders may also insist on shorter tenures or additional safeguards, depending on internal credit policies.

Why EMI Planning Matters

Many EMI bounces occur not due to lack of income, but due to poor cash flow planning. Misaligned salary dates, multiple active EMIs, or underestimating monthly expenses are common reasons.

This is why planning EMIs properly is critical. Using an EMI calculator helps estimate affordable monthly repayments in advance, align EMIs with income cycles, and reduce the risk of future payment failures.

Proactive EMI planning not only protects your credit score but also improves long-term loan eligibility across banks and NBFCs.

Do EMI Bounces Lead to Recovery Calls or Legal Action?

In most cases, a single EMI bounce does not result in recovery calls or legal action. Lenders usually begin with reminders through SMS, email, or calls to inform borrowers about the missed payment.

Recovery actions or legal proceedings are typically considered only in cases of repeated or prolonged defaults, and are carried out as per lender policy and applicable regulations.

Borrowers who address EMI issues promptly and communicate with the lender can usually avoid escalation.

What Should You Do Immediately After an EMI Bounce?

If an EMI bounce occurs, acting quickly can help limit financial penalties and reduce long-term impact on your credit profile. The steps below explain what you should do immediately.

✔ Maintain Sufficient Balance

Ensure your linked bank account has enough funds as soon as possible. Many lenders attempt re-presentation of the EMI within a few days. Maintaining sufficient balance increases the chances of successful debit.

✔ Pay Bounce Charges Promptly

Clear any applicable EMI bounce charges and overdue amounts without delay. Prompt repayment can reduce penal interest and may limit the negative impact on your credit score.

✔ Contact the Lender Immediately

If the EMI bounce was due to a genuine reason such as salary delay or technical issues, inform the lender proactively. Early communication can help prevent escalation to recovery follow-ups.

✔ Avoid Repeated EMI Failures

Repeated EMI bounces signal repayment stress to lenders. Make sure future EMIs are honoured on time to avoid stricter actions, additional charges, or adverse credit reporting.

✔ Review EMI Affordability

If EMIs feel difficult to manage, reassess your repayment capacity. Reviewing your monthly budget and using tools like EMI calculation can help determine a more sustainable EMI amount.

✔ Align EMI Date With Income Cycle

Where possible, request the lender to align your EMI due date with your salary or income credit date. This simple adjustment can significantly reduce the risk of future payment failures.

Taking timely corrective steps after an EMI bounce not only helps control immediate penalties but also protects your long-term credit health and future loan eligibility.

How to Avoid EMI Bounce in the Future

- Maintain a buffer balance before EMI date

- Align EMI date with salary credit date

- Track active EMIs and due dates

- Avoid over-borrowing beyond repayment capacity

Simple financial planning steps can prevent unnecessary penalties and protect your credit profile.